Social Security and Retirement Contributions (SSRC) Plan

This essay was entered into the iOme Challenge and won runner up. The link to the challenge’s past winners is here: https://iomechallenge.org/past-challenges/

Brennan Dwyer

1. Introduction

1.1 Introduction to Problem

There is currently a retirement crisis in the United States of America. This includes retirement programs like Social Security, and the retirees themselves. For one, Social Security will soon be paying more out than what it is bringing in. “Starting in 2021, Social Security’s total cost will exceed its total income” -as stated by cbpp.org (Policy Basics: Understanding the Social Security Trust Funds, 2020). As stated by iomechallenge.org, “Current projections indicate that unless changes are made to either or both the funding and benefit payments, Social Security will only be able to pay 75 percent of benefits starting in 2035” (https://iomechallenge.org/). Also, despite the fact that employee-sponsored retirement plans not only increase the likelihood of the workers contributing to retirement but also help match up towards the amount saved for retirement, many workers still do not participate in a plan (https://iomechallenge.org/). Not only are many workers not participating in a plan, they aren’t saving very much for retirement to begin with. According to pbs.org “Nearly half of Americans nearing retirement age (65 years old) have less than $25,000 put away, according to the Employee Benefit Research Institute’s annual survey” (Frazee 2018)

1.2 Introduction to Proposal

This proposal describes a bipartisan solution for the retirement crisis titled the “Social Security and Retirement Contributions (SSRC) Plan.” The Social Security fund clearly isn’t receiving enough revenue, and not all income levels contribute the same amount to the Social Security fund. This proposal will focus on having all income levels contribute the same rate for Social Security by removing the maximum taxable earnings for Social Security. The amount of revenue created from these new contributions will be from upper incomers, with the revenue used as an incentive for other income level groups to save for retirement. More specifically, the lower to middle income class would be given cash payments from the additional mentioned revenue above, with the caveat that they must contribute a set minimum amount for retirement. This will hopefully encourage people to invest for their retirement and be less reliant on the Social Security fund that is running out. It is important that this idea is a bipartisan one, because otherwise it might never go through if there isn’t support from both parties. So, part of the compromise will also include having a larger share of the Social Security fund invested in the stock market for higher long-term returns. If more of the money put towards the Social Security fund is gradually put in the stock market, then hopefully the returns for Social Security will likely be higher and make the Social Security fund not face major issues in the future. Finally, part of the compromise that both parties may agree upon, is having a requirement where high school students must take a personal finance or economics class.

2. Social Security and Retirement Contributions (SSRC) Plan

This proposal suggests a bipartisan solution, as bipartisanship is very important. Like in many issues in politics, very little will likely get done unless there is compromise between both Republicans and Democrats. The bipartisan proposal is titled the “Social Security and Retirement Contributions (SSRC) Plan”.

2.1 Removing the Maximum Taxable Earnings for Social Security

Part of the proposal is to have all income levels contribute the same rate for Social Security, while using that extra money from the upper incomers contributing to give cash payments to lower and middle income class Americans if they contribute a certain amount for retirement. From “ssa.gov”, The income that is the maximum taxable earnings for Social Security as of 2016 was “$118,500” a year (Retirement Benefits Maximum Taxable Earnings). From looking at the “Summary of Federal Income Tax Data” for 2016 the income split point for the top 10% is about “$139,713”, which isn’t a value too far off from the maximum taxable earnings for that year (Bellafiore, 2018). Interestingly, the “gross adjusted annual income” for the top 10% is “$4,729,405” in millions, (which is over 4.7 trillion dollars a year) (Bellafiore, 2018). That makes up a large portion of the overall adjusted gross income of all taxpayers, which is “$10,156,612” in millions, (or over 10.1 trillion dollars a year) (Bellafiore, 2018). If the top 10% all paid exactly the 6.2 percent required for Social Security, and their employees paid the 6.2 percent required to match up for it, then 12.4 percent of $4,729,405 in millions is about $586.4 billion. (It should be noted that the top 10% already does pay some income towards Social Security, but obviously not the full amount that is currently suggested because of the Maximum Taxable Earnings for Social Security. For example, someone making a very high income may be paying 3% of their income towards Social Security, as opposed to the 6.2%) The point of this calculation is that the top 10% of taxpayers (which is a little more than the maximum taxable earnings for Social Security) makes up a large share of the income for all taxpayers, and therefore a requirement for everyone to pay the 6.2 percent for Social Security, as well as their employees paying 6.2 percent as well, would bring in quite a lot of revenue. All the extra revenue is suggested to go towards paying lower to middle income Americans who contribute a certain amount for retirement, so that they have a short-term incentive to do so. This is especially considering that many people likely think in the short term, and not just in the long term.

Human behavior is always an important thing to consider. There is something called “hyperbolic discounting”, which is basically where people choose short term rewards over later rewards that may be larger. This may very well apply to saving for retirement, and perhaps why many people are not saving, or saving enough for retirement. According to the paper titled “Increasing Saving Behavior Through Age-Progressed Renderings of the Future Self”, “research on excessive discounting of the future suggests that removing the lure of immediate rewards by precommitting to decisions or elaborating the value of future rewards both can make decisions more future oriented” (Hershfield.). Interestingly, the paper found that “In four studies, participants interacted with realistic computer renderings of their future selves using immersive virtual reality hardware and interactive decision aids. In all cases, those who interacted with their virtual future selves exhibited an increased tendency to accept later monetary rewards over immediate ones” (Hershfield). It is definitely important to consider how people think in short term and long term, and what might incentivize people to actually save long term for retirement. This proposal tries to focus on this.

Regarding the specific amount paid to lower to middle income Americans, is it would obviously depend upon the amount of revenue actually generated from requiring all levels of incomers to pay the same amount in Social Security as a percentage. An example could be for every $3 that someone in the bottom 50% of household income contributes to retirement, they get $1 dollar to spend on whatever they want. This can work for up to a certain amount, such as $2,000. Part of the calculation would obviously be to calculate what percentage of Americans would actually follow through and contribute to retirement, so that it can be calculated how much money can be given to those that contribute, since the amount will be limited to the amount of revenue from the increase in the Social Security taxes on the upper incomers.

One estimate that was done on how much taxes there would be from elevating the cap with the Social Security tax (which would likely also mean how much revenue for the government) was done by the Heritage Foundation “based on data from the SSA” (Wilson & Davis). Even though this article was written in 1999, it did estimate that “eliminating the cap in wages would” cause an increase in taxes by “$425.2 billion in nominal dollars over five years.” (Wilson & Davis). That number of taxes/revenue would obviously be much larger today, because of inflation and the increase of wages, especially as upper incomers have seen significantly larger increases in income compared to middle income Americans (as the upper incomers are the bracket of incomers that would see an increase in taxes).

One thing that fiscally conservative Republicans may like about this idea is that it will incentivize lower to middle income Americans to be less dependent on government programs like Social Security, which the Republicans would support. The Republicans often seem to emphasize a more balanced budget and the importance of not increasing the national debt, and so if more lower and middle incomers are less dependent on Social Security, then that means that it would be less of a problem with having to increase the Social Security spending that may require more national debt. The Democrats would support the aspect of all income levels contributing to Social Security, and the money being given to the lower to middle income class Americans.

2.2 Social Security Fund Gradually Invested in Stock Market

Part of the compromise which may be more supported by Republicans would be having a gradual shift towards a larger share of the Social Security fund invested in the stock market for higher long-term returns. Even President Bill Clinton briefly brought up the idea of it (Munnell & Tanner, 2017).

As stated by investopedia.com, “The Social Security Trust Fund has no direct connection to the stock market.” (Daugherty, 2020). This is important to realize, as Social Security has very little returns compared to the stock market. Considering that Social Security is invested in government bonds, and that the equity premium (difference in returns between the U.S stock market and U.S Government bonds) is about 6 percent, then clearly the U.S stock market is a better investment in the long run. However, there is obviously risk in the stock market, and the stock market is especially riskier then U.S Government bonds.

For this proposal, it was even further investigated just how much stocks returns more than bonds, despite stocks being risker then bonds.

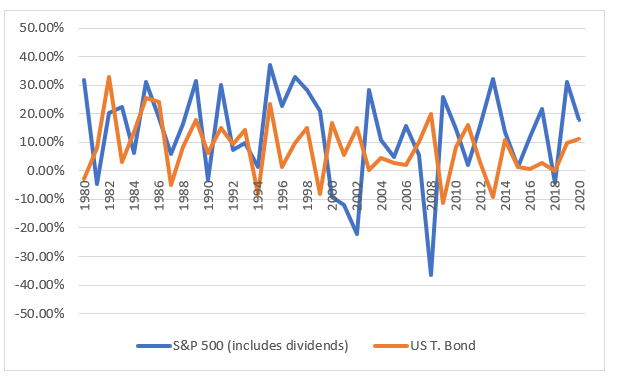

Figure 1 shows the annual returns of the S&P 500 (a popular U.S index fund) including dividends, and US. Treasury bonds from 1980-2020.

Figure 1: Annual returns of the S&P 500 including dividends, and US. Treasury bonds from 1980-2020. Data from stern.nyu.edu (Historical Returns on Stocks, Bonds and Bills: 1928-2020).

Figure 1 clearly shows that despite some exceptions, overall, the index fund S&P 500 plus dividends tends to have much higher returns than U.S treasury bonds.

Using that date for Figure 1 from stern.nyu.edu, the average yearly return between 1980-2020 for the S&P 500 including dividends was 13.11%, and for U.S treasury bonds it was significantly lower, at a value of 7.93 percent. This somewhat helps verify the earlier statement that the equity premium between stocks and bonds is about 6%.

Figure 2 visualizes the difference between the average yearly return between 1980-2020 for the S&P 500 and for U.S treasury bonds. Again, the data was taken from stern.nyu.edu (Historical Returns on Stocks, Bonds and Bills: 1928-2020).

Figure 2: average of the annual returns of the S&P 500 including dividends, and US. Treasury bonds from 1980-2020. Data from stern.nyu.edu (Historical Returns on Stocks, Bonds and Bills: 1928-2020).

So, based on what is shown in Figure 1 and Figure 2, it is safe to say that stocks not only return significantly more than bonds, but also by a large amount in recent times (over the past decades). As stated before, it should be reminded that the data was taken from stern.nyu.edu (Historical Returns on Stocks, Bonds and Bills: 1928-2020).

It should be noted that the standard deviation was found using the “Data Analysis” tool on Excel, and the “confidence level for mean” was 95%. From using the data on Figure 1 and Figure 2, it was found that stocks have a much higher standard deviation then bonds. More specifically, for the yearly S&P 500 including dividends from 1980-2020 was 0.161357, and for U.S treasury bonds it was 0.099454. This means that stocks are much risker then bonds, because of the larger standard deviation. This is no surprise, as general research in financial economics states how stocks have much more volatility and risk then bonds. As stated by a financial economics paper titled “THE EQUITY PREMIUM: WHY IS IT A PUZZLE?”: “The standard deviation of the returns to stocks (about 20 percent a year historically) is larger than that of the returns to T-bills (about 4 percent a year), so obviously, stocks are considerably riskier than bills” (Mehra, 2003).

So considering the greater risk of stocks then bonds found by this paper and based on the general consensus of financial economics research, the shift towards having a portion of the Social Security in the stock market should be a gradual one, perhaps with only having the additional money brought in for Social Security starting this year to act as the money that is put towards the stock market, and have none of the money already in Social Security from previous years be put in the stock market. Other proposals for having some of the Social Security funds invested in the stock market also propose having it as a gradual adjustment (Munnell & Tanner, 2017). According to an article on MarketWatch “Those pushing to diversify Social Security’s holdings have called for investing only a portion of the trust fund in stocks. The typical proposal would increase the percentage of the trust fund invested in stocks by 2 to 3 percentage points annually until stocks accounted for 40% of total Social Security assets” (Munnell & Tanner, 2017).

One important aspect of the stock market that should be noted, is how the stocks tend to go up due to further demand. Considering that the wealthy own such a large share of the stock market, they are likely the ones that cause a large amount of the demand for stocks, which causes the prices to go up. Because of this, if there was suddenly a wealth tax, that could cause the wealthy to sell parts of their stocks, which may cause less of an increase in prices for the stock market, which could mean less returns for everyone. One way to look at it is that theoretically, the wealthy are the ones that buy stocks and keep it in the stock market and see their wealth grow, as opposed to the middle class that invests in the stock market and eventually withdraw a large portion of it over their retirement. So, though wealth inequality is often seen as a bad thing, there is the upside of the wealthy having a growing net worth by having their money invested in the stock market, and not withdrawn. Therefore, a wealth tax should be avoided.

2.3 Personal Finance or Economics as Mandatory High School Class

Finally, part of the compromise should be to have all high school students take a mandatory personal finance or economics class. The personal finance class should obviously teach the importance of saving for retirement early, how to save for retirement and the different contributions plans, and how employers often match up with retirement contributions. It should also teach the concept of compound interest, and how that relates to retirement savings. To add a little bit of flexibility to the policy of having a mandatory personal finance class taken by all high schools students, is that economics as a class can be substituted for that, since it also teaches important lessons that may relate to personal finance.

According to an opinion article on MarketWatch, “In 23 states and the District of Columbia, less than 5% of students during the 2018-2019 school year were required to take a stand-alone personal-finance semester” (Ranzetta, 2019). This is obviously very concerning, and again why there should be a national law that all high school students are required to take a personal finance class, or at least something similar in place of a personal finance class, like economics. Another concern that the article brought up is that only a small portion of teachers are actually qualified to teach personal finance, specifically when looking at the amount that have “taken a college course offering personal finance” (Ranzetta, 2019). So if there were to be a national law that requires all students to take a personal finance class or an economics class as an alternative, then if a school doesn’t offer it because of a lack of qualified teachers to teach it, then it should be ensured that all students have access to some form of online school that teaches personal finance (or economics as an alternative). On the other hand, the article on MarketWatch did explain how the majority of teachers are willing to do “formal financial-education training” (Ranzetta, 2019). So, if there is more investment towards making teachers qualified to teach personal finance, then many schools might not need to have a form of online schooling for the students to learn personal finance. Perhaps the investment towards making teachers qualified to teach personal finance can come from the federal government.

3. Conclusion

In conclusion, there is a large retirement crisis that needs an urgent solution. This proposal not only addresses how it can be fixed in different ways, but also explains with great simplicity, and most importantly is intended to be a proposal that would act as a bipartisan compromise. If a proposal for a solution for the retirement crisis isn’t bipartisan, then it likely won’t even pass, or at least not for the long run.

This proposal had three main suggestions. The first and largest suggestion was for all income levels to contribute the same rate (in percentage) for Social Security by removing the maximum taxable earnings for Social Security. That would mean that someone making $200k a year would be paying the same percentage of their income towards Social Security as someone making $20K a year. However, the additional revenue from this change will go towards giving cash towards middle to lower income households if they contribute a given amount for retirement, as an incentive to save for retirement. The second suggestion was to gradually have more of the Social Security fund invested in the stock market. Finally, the final suggestion was to have a required personal finance class for all high school students, or an economics class taken as an alternative.

Hopefully this proposal will help many retirees, and the United States of America as a whole.

Bibliography

Background. iOme Challenge. https://iomechallenge.org/background/.

Bellafiore, R. (2018, November 13). Summary of the Latest Federal Income Tax Data, 2018 Update. Tax Foundation. https://taxfoundation.org/summary-latest-federal-income-tax-data-2018-update/.

Daugherty, G. (2020, August 28). How Is the Social Security Trust Fund Invested? Investopedia. https://www.investopedia.com/ask/answers/110614/how-social-security-trust-fund-invested.asp.

Frazee, G. (2018, June 13). The numbers you need to know about the retirement crisis. https://www.pbs.org/newshour/economy/making-sense/the-numbers-you-need-to-know-about-the-retirement-crisis#:~:text=%2425%2C000%3A%20Nearly%20half%20of%20Americans,should%20save%2C%20retirement%20experts%20say.

HAL E. HERSHFIELD, DANIEL G. GOLDSTEIN, WILLIAM F. SHARPE, JESSE FOX, LEO YEYKELIS, LAURA L. CARSTENSEN, and JEREMY N. BAILENSON. Increasing Saving Behavior Through Age-Progressed Renderings of the Future Self. vhil.stanford.edu/. https://vhil.stanford.edu/mm/2011/hershfield-jmr-saving-behavior.pdf.

Historical Returns on Stocks, Bonds and Bills: 1928-2020. Welcome to Pages at the Stern School of Business, New York University. http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html.

Mehra, R. (2003, February 24). The Equity Premium: Why is it a Puzzle? NBER. https://www.nber.org/papers/w9512.

Munnell, A. H., & Tanner, M. D. (2017, April 18). Should the Social Security fund be invested in the stock market? It’s complicated. MarketWatch. https://www.marketwatch.com/story/should-the-social-security-fund-be-invested-in-the-stock-market-its-complicated-2017-04-18.

Policy Basics: Understanding the Social Security Trust Funds. Center on Budget and Policy Priorities. (2020, May 14). https://www.cbpp.org/research/social-security/policy-basics-understanding-the-social-security-trust-funds#:~:text=The%20Social%20Security%20trust%20funds%20are%20invested%20entirely%20in%20U.S.,credit%20of%20the%20U.S.%20government.

Ranzetta, T. (2019, September 23). Opinion: Why do so many U.S. schools ignore personal-finance education? Here’s an answer… MarketWatch. https://www.marketwatch.com/story/want-to-develop-financially-capable-americans-teachers-may-be-even-more-important-than-laws-2019-09-20.

Retirement Benefits Maximum Taxable Earnings. ssa.gov. https://www.ssa.gov/benefits/retirement/planner/maxtax.html.

Wilson, D., & Davis, G. The Impact of Removing Social Security’s Tax Cap on Wages. The Heritage Foundation. https://www.heritage.org/social-security/report/the-impact-removing-social-securitys-tax-cap-wages/#pgfId=1002931.